Zagreb’s Open Gym Market: A Whitespace Analysis

Identifying whitespace in Zagreb’s open gym market requires navigating a mature and segmented landscape. The city spans budget-tier operators, premium clubs, wellness-integrated facilities with secondary gym spaces, and multi-sport complexes that bundle exercise offerings alongside other amenities. With 94 open gyms (i.e. facilities that permit independent, unguided exercise) and a further 67 street-workout parks, Zagreb’s fitness infrastructure has reached a mature stage of development.

Furthermore, this maturity is also evident from the shift toward higher-utilization of open gym formats in recent market development. National chains such as Gyms4You and THE Fitness have expanded by offering members access across multiple locations under a single subscription, increasing convenience, network flexibility, and effective catchment reach. At the same time, the growing role of the MultiSport network has further reshaped consumer behavior. Under this model, employers subsidize employee memberships, while users pay a reduced monthly fee and gain access to participating fitness facilities once per day. This has lowered effective price sensitivity for part of the market and increased substitutability between gyms (and other fitness facilities) within the same access network.

Whether this supply adequately serves a city of roughly 800,000 residents, however, remains an open question — and one worth interrogating to surface unmet demand.

Geographical overview

As noted, Zagreb currently hosts 94 open gyms across several parts of the city. The aggregate count alone, however, offers limited insight. The more pertinent question is whether supply is evenly distributed, or concentration patterns point to underserved areas worth capturing.

To surface this, the market is best viewed through the lens of Zagreb’s 18 local districts. This framing enables identification of both density hotspots and geographical whitespace. The illustration below maps gym locations and heat concentrations across the city.

Zagreb Gym Location by District

Source: Google Maps; Everest One analysis

District-level analysis shows that gym demand in Zagreb is shaped not only by district size, but also by other drivers. Northern districts in particular require differentiated interpretation. These districts typically include elevated residential areas with lower concentrations of daily work-related footfall. Their road networks are often oriented predominantly north–south, which can make east–west movement less efficient and increase travel time between parallel corridors. In practical terms, this means residents often gravitate either toward gyms located at the lower edge of these elevated zones—where the denser urban fabric begins—or toward facilities near their workplace. As a result, the upper residential parts of northern districts generally support fewer open gyms. Where facilities are present, they are more often positioned as multi-sport complexes or destination-led formats that draw from a wider catchment area rather than relying solely on immediate neighborhood demand. The extent of this dynamic varies by district depending on the share of elevated residential territory within its boundaries.

A separate but equally relevant consideration is the degree of urbanization. Peripheral districts with lower residential density and more fragmented built form tend to support different demand economics. Brezovica is a clear example: the district is characterized predominantly by family housing, limited multi-storey residential stock, and currently no open gyms. While urban density differs across peripheral districts, lower-density environments generally imply weaker immediate catchment, greater car dependence, and a higher threshold for standalone gym viability.

From a citywide perspective, open gym supply is distributed primarily along an east–west urban axis. The highest concentration is visible in Donji Grad and Trnje, which together form Zagreb’s central business and residential core. Among non-central districts, Stenjevec and Trešnjevka sjever stand out as relatively gym-dense markets, with open gym supply distributed relatively evenly across both districts respectively. By contrast, the remaining districts contain visible pockets of limited supply. The natural question follows: do these gaps represent genuine opportunity?

A first-order answer demands caution. Empty territory is not necessarily underserved territory. It may simply be underpopulated. Peščenica-Žitnjak, for instance, extends across cca. 35 km² with a resident population of cca. 49.100, whereas Donji Grad covers cca. 3 km², yet houses around 34.200 residents. Given that the latest population census was conducted in 2021, all population figures refer to 2021 census data. Therefore, before deeper analysis, geographic whitespace must be normalized against population. A more rigorous approach calculates gyms per resident at the district level.

As the table indicates, some districts that display significant visual whitespace do not necessarily carry large population bases. Assessing the relationship between district population and existing gym count therefore provides a more reliable first filter for identifying potential opportunity areas. However, translating that into actionable market opportunity requires a second layer of spatial assessment—specifically, understanding whether the mentioned visual gaps fall within low-density residential zones dominated by family housing or within more urbanized, higher-catchment areas. This distinction is examined further in the Market Opportunity section.

Source: Population data based on DZS Census 2021

Pricing

As flagged earlier, open gyms in Zagreb take varied forms. Some of them are standalone fitness facilities while some are multi-purpose complexes that pair exercise space with sports courts, boxing rings, or wellness amenities. Equipment quantity and quality, footprint, and location all factor into membership pricing.

The MultiSport network also plays an important role in shaping the pricing landscape. While many open gyms monetize through a mix of memberships, group classes, and individual training services, facilities with MultiSport contracts remain accessible under a different pricing logic. Under this model, users typically pay a subsidized monthly fee—generally in the range of €20–50, depending on employer contribution—and are able to access participating open gyms (and other fitness facilities) once per day. This lowers effective price sensitivity for a meaningful share of users and increases substitutability between gyms operating within the same access network.

Nevertheless, reviewing standard monthly membership prices remains important, as it provides a useful indication of consumer willingness to pay and helps define potential positioning for a new open gym. To map the pricing landscape, monthly rates were collected from 84 of the 94 gyms; the remaining 10 do not publish prices publicly. Across the sample, monthly memberships range from €28 at the low end to €135 at the top creating a spread of nearly 5x. Given the breadth of this range, two pricing categories are defined below.

The lower end of the budget segment (€28–35) is typically occupied by independent, small-footprint operators or by businesses whose primary activity lies outside core gym operations. One example is Embassy Gym, operated by Padel Embassy, where fitness functions as a complementary offering alongside the core padel business.

The 45–55€ price band represents the most competitively contested segment of Zagreb’s open gym market, populated by national chains such as Fitness Forma and Gyms4You alongside strong independent operators. Companies in this segment typically use tiered membership structures—including annual contracts, six-month memberships, off-peak access packages, and pensioner plans—to broaden price accessibility and attract different customer segments. For example, Gyms4You offers an annual contract priced at 318€, which translates to an effective monthly fee of 26,50€.

Within the premium tier (€65+), the €65–80 sub-band is the most densely occupied. This category is predominantly held by national chain The Fitness, priced exactly at 65€. Besides offering open gym services, The Fitness also offers sauna facilities, which allows price increase and premium positioning.

At 135€ there is WorldClass, operating in two locations, Hilton and Sheraton. Alongside their positioning deep in the city’s center, in the spaces of two premium hotels, WorldClass gyms are defined by high-end design, sauna and pool facilities, lounge areas, and elevated hygiene and service standards.

Market Opportunity

To identify actionable market opportunities, the analysis does not rely on visual supply gaps alone, as spatial whitespace by itself can be misleading. Instead, districts are filtered through a demand-capacity lens that compares estimated potential member base against the existing number of open gyms. The underlying logic is straightforward: the greater the number of potential members each gym must serve, the greater the likelihood of unmet demand.

As the number of open gyms by district is already established, the remaining variable is the potential member base. This is estimated by converting 15+ years old population district population into gym-active population using a 10.6% penetration rate (EuropeActive, 2024). A fully precise catchment analysis would also account for non-resident daily flows—such as commuters, students, and tourists—but for analytical consistency and comparability, this assessment is limited to resident population.

Pricing is incorporated as a complementary layer of analysis. Reviewing the pricing landscape at district level helps assess not only local willingness to pay, but also the prevailing market positioning within each district. This provides a clearer view of where current supply is concentrated and where an entrant may choose to position differently by addressing underrepresented pricing segments or value propositions. Average district-level price, however, can be misleading, as a single premium outlier may materially skew the mean. A more reliable read comes from assessing the share of budget and premium gyms operating within each district. The illustration below synthesizes both dimensions to surface the districts offering the strongest entry conditions.

Market Saturation: Number of Gyms vs. Potential Members

Source: Population data based on DZS Census 2021; Everest One analysis

As shown in the chart above, several districts emerge as potential opportunity areas, with estimated potential member base per open gym ranging from roughly 400 to nearly 2,500. To focus the analysis on structurally less saturated markets, the priority set is limited to districts where each open gym serves more than 1,000 potential members. On this basis, the relevant districts are Podsused–Vrapče, Trešnjevka jug, Črnomerec, Gornja Dubrava, and Novi Zagreb-istok.

However, potential member load alone does not fully determine attractiveness. As outlined in the geographic overview, several of these districts include elevated residential areas that are typically less urbanized, attract fewer work commuters, and are characterized by mobility patterns that make cross-district movement less efficient. This is particularly relevant for Črnomerec and Gornja Dubrava. While Črnomerec, and Gornja Dubrava also contain more urbanized lower sections, those areas already exhibit relatively dense open gym coverage, which reduces the practical attractiveness of their headline demand figures.

For this reason, despite higher nominal unserved demand in some of those districts, Novi Zagreb-istok—with approximately 1,280 potential members per open gym—emerges as a more attractive opportunity from a market-access perspective. Podsused–Vrapče also stands out. Although the district includes elevated residential territory, it contains visible supply gaps in its more urbanized, non-elevated sections and records the highest estimated unmet demand in the city, with approximately 2,480 potential members per open gym. Finally, Trešnjevka jug—which does not contain elevated residential areas within its boundaries—currently supports roughly 1,800 potential members per open gym, reinforcing its position as one of the more compelling whitespace opportunities. Additionally, although Brezovica district counts 0 gyms, it will be excluded from the further analysis due to its low level of urbanization.

Regarding pricing, as noted earlier, 10 open gyms do not publicly disclose membership fees and are therefore excluded from district-level pricing analysis. This affects Podsljeme, Donja Dubrava, Peščenica–Žitnjak, Trnje, Novi Zagreb-zapad, Sesvete, Črnomerec, and Gornja Dubrava, meaning that the observed pricing mix in these districts should be interpreted as directional rather than exhaustive.

Based on the available data, Podsused–Vrapče, Maksimir, Novi Zagreb-istok, and Podsljeme currently present as fully budget-oriented open gym districts. Most remaining districts include at least some premium presence within their local mix. This is driven in large part by the footprint of THE Fitness, whose multi-district presence has introduced a consistent premium reference point at the €65 price level across the city.

Donji Grad stands out as the most premium district in Zagreb. Positioned in the city’s center, 57% of its open gym portfolio is priced above €64. The district also contains both locations of World Class, which at €135 represent the upper end of the city’s pricing spectrum.

Although this overview is giving us a good idea which districts should we look at when considering opening an open gym, and also allows us to know what is currently the most common pricing positioning in each district, it doesn’t explain who are the current players, what are they missing, or what exactly is their pricing. This is why the following section will give a short overview of 3 high opportunity districts:

- Podused-Vrapče

- Trešnjevka-jug

- Novi Zagreb-istok

1. Podsused-Vrapče

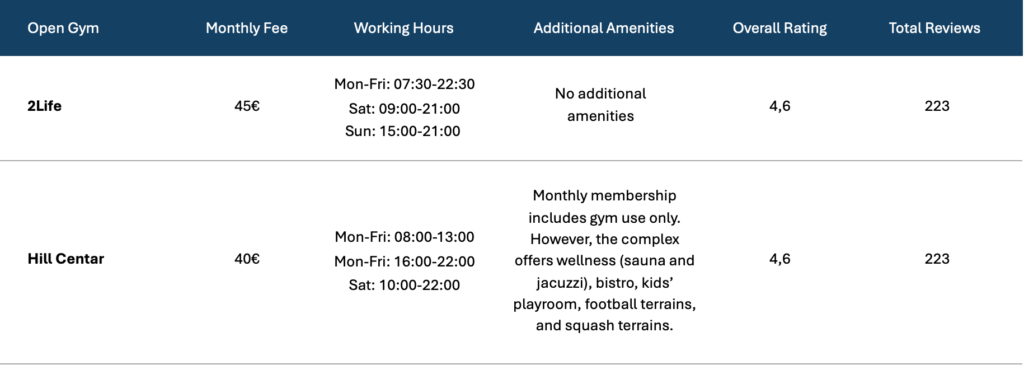

Podsused–Vrapče records the lowest gym density of any populated district in Zagreb, with two operators serving a potential member base of approximately 4,200. Located in the western part of the city, the district includes a substantial share of elevated residential territory. However, the more urbanized section currently accommodates only one open gym—2Life—which leaves a clear location-based opportunity within the district’s denser residential fabric.

The second operator, HILL CENTAR, is positioned in the elevated part of the district. As noted earlier, operators in these elevated residential areas often rely on broader destination appeal rather than purely local gym demand. HILL CENTAR follows this pattern by operating as a multi-sport complex that combines gym facilities with additional amenities, including a bistro, helping it attract a wider audience beyond core gym users. Please find the competitive overview in the table below.

Source: Everest One analysis

Both 2Life and HILL CENTAR are positioned within the budget segment and maintain strong review scores above 4.0. It should be noted, however, that HILL CENTAR’s reviews relate to the broader multi-sport complex rather than exclusively to the gym itself, which makes it difficult to isolate sentiment toward the open gym offering alone. On the other hand, 2Life also operates within the MultiSport network, which strengthens its competitive position by increasing accessibility for users whose memberships are employer-subsidized.

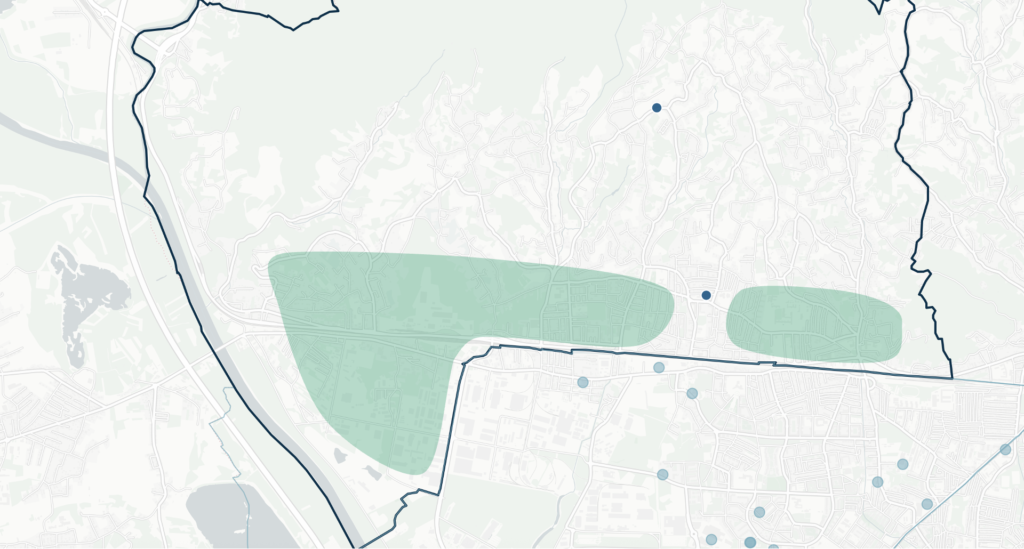

At first glance, combining the strengths and addressing the gaps of both operators may appear to suggest a natural positioning strategy. In practice, this may not be necessary. The primary opportunity lies in the more urbanized lower part of the district rather than in competing directly with the structural challenges of the elevated residential areas. The more relevant question is therefore where spatial whitespace remains concentrated within the district. Please refer to the map below for the identified opportunity areas.

Source: Everest One analysis

The highlighted areas indicate the more urbanized parts of the district, where east–west connectivity is stronger and road structure allows more efficient local access compared with the elevated residential zones. From a consumer perspective, these areas offer more practical gym accessibility and therefore represent the most attractive catchment for a new entrant.

From a positioning standpoint, a budget concept, included in the MultiSport network, appears the most natural starting point. As a peripheral district, Podsused–Vrapče remains more dependent on residential demand than on commuter-driven footfall. At the same time, there is room for selective differentiation. A lower-premium concept positioned around the €65 price point, supported by additional amenities, could establish a stronger competitive foothold by offering a proposition that is currently underrepresented within the district. However, a more granular residential analysis would be required to fully validate local willingness to pay for premium services.

It should also be noted that several open gyms are located in the upper area of the southern neighboring Stenjevec. However, the railway corridor acts as a meaningful local barrier, reducing ease of cross-district movement and preserving the practical whitespace within Podsused–Vrapče.

2. Trešnjevka – jug

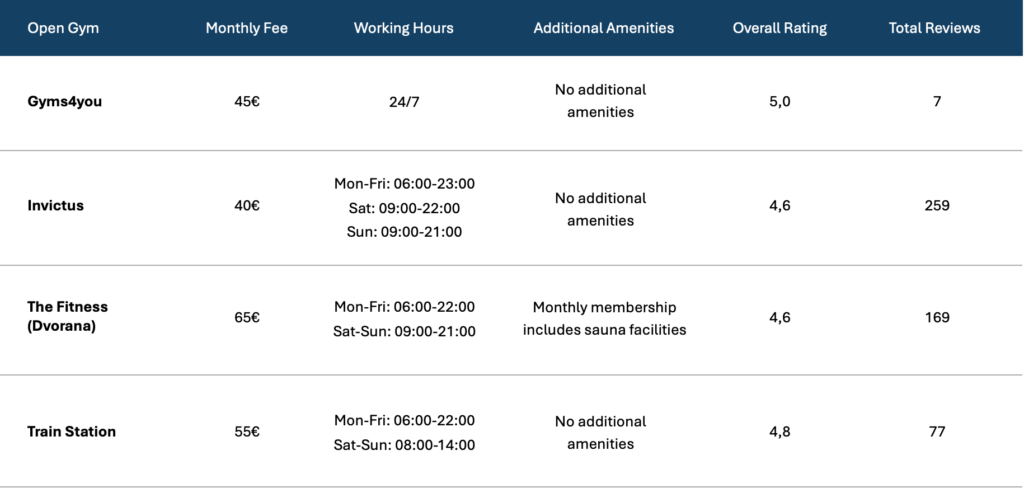

Trešnjevka–Jug is served by four open gyms against a potential member base of approximately 6,265. Current supply is concentrated in the north-western part of the district, creating a localized cluster of competitive intensity while leaving other parts of the district comparatively less served. The recent opening of Gyms4You in the same building as THE Fitness is likely to reshape local competitive dynamics. This is particularly relevant given that all four current operators participate in the MultiSport network, allowing subsidized users to move between participating gyms with relatively low switching friction. Please find the competitive overview below.

Source: Everest One analysis

All four operators maintain strong review scores. THE Fitness and Gyms4You further benefit from national brand recognition and a relatively standardized customer proposition across locations. Their citywide footprint creates an additional competitive advantage beyond the MultiSport network, as members can use multiple locations across Zagreb under a single membership, increasing convenience and effective catchment flexibility.

From a pricing perspective, the district also contains two premium-positioned operators, which further intensifies competition. One of these, THE Fitness, strengthens its premium positioning through the inclusion of sauna facilities. Taken together, the north-western part of Trešnjevka–jug already combines established brands, network access, and a broad pricing mix, making direct entry into this cluster comparatively challenging. The more relevant strategic question is therefore where spatial whitespace remains within the district. Please refer to the map below for the identified opportunity areas.

Source: Everest One analysis

Although the north-western part of Trešnjevka–jug is already clustered, the map still reveals several pockets of unmet demand. A smaller whitespace area is visible in the far western part of the district, but this would likely be more challenging to capture given the proximity of multiple operators in neighboring Stenjevec and Trešnjevka-sjever.

The eastern pocket appears materially more attractive. This area offers flexibility in positioning, with both budget and premium entry strategies appearing viable. The far eastern edge of the district includes a student dormitory catchment, which suggests that a monthly subscription in the €40–45 range, supported by dedicated student packages, would likely represent the most natural fit for that micro-market.

At the same time, the broader eastern whitespace extends beyond the immediate student catchment. This opens additional opportunities in the more central part of the highlighted area, where premium positioning may also be commercially credible. Existing willingness to pay at the €65 level has already been demonstrated locally by Invictus and THE Fitness, indicating that a differentiated higher-value proposition could also be absorbed by the market.

3. Novi Zagreb – istok

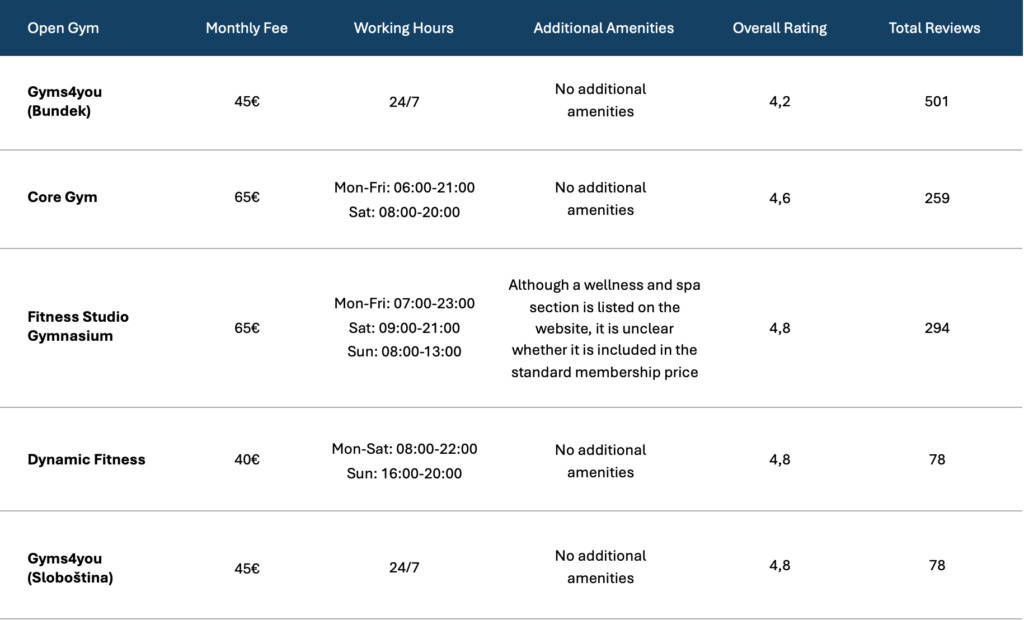

Novi Zagreb-istok includes five gyms serving a potential member base of approximately 5,604, making it the last district in the analysis with more than 1,000 potential members per gym. Although positioned in the southern part of Zagreb and therefore classified as a peripheral district, its gym landscape already includes one premium open gym, alongside budget-oriented operators. This creates a relatively diverse and mature competitive structure despite its peripheral location. Please review the competition table below.

Source: Everest One analysis

Although there is a presence of national chain Gyms4you, its both locations currently hold the weakest rating in the district. Besides Gyms4you there is Core Gym, with its spaces including the boxing rings and small running trails, and strong branding within the locality of the district, allowing the low-end of premium pricing at 65€. Fitness Studio Gymnasium and Dynamic Fitness are both positioned as budget gyms. Both Gyms4you, Fitness Studio Gymnasium and Dynamic Fitness are included within the MultiSport network, increasing their competitiveness in that way as well and leaving the Core Gym as the only player outside the MultiSport network inside the district. All in all, the district is, in the urbanized area, somewhat mature. Let’s review the map to see the potential gaps.

Source: Everest One analysis

By reviewing the map, there are multiple areas empty of gyms: north central area, east area, and south area. However, the east and the south area are mostly family houses and are less urban, reducing the potential catchment in that area. This leaves us with the central north. In this part, large residential buildings are very common, increasing the catchment a lot. Positioning a highly equipped budget gym at the price range of 40-50€ would at the same time allow being a direct competitor to both budget operators but to Core Gym as well. To further improve that competitiveness, inclusion in MultiSport network would make a new gym more competitive in relation to current budget gyms, but offer additional benefits in comparison to the premium player as well.

Conclusion

Overall, although Zagreb’s fitness landscape is relatively mature, multiple districts still present viable expansion opportunities, most notably Podsused–Vrapče, Trešnjevka–jug, and Novi Zagreb–istok. This analysis excluded positioning assessment in certain elevated areas across several districts; however, this should not be interpreted as an absence of opportunity. Rather, successful entry into such locations would likely require differentiated positioning, potentially supported by multi-sport facilities or elevated design concepts tailored toward wealthier residential catchments. Such positioning could also justify entry into already saturated gym clusters by targeting consumers seeking a more distinctive fitness experience.

It is also important to acknowledge the growing momentum of the premium gym segment. The continued expansion of The Fitness, operating at approximately 65€ monthly membership fees, demonstrates that higher pricing supported by additional amenities can sustain demand. Similarly, World Class has reinforced this trend through the opening of its second Zagreb location, despite memberships priced around 135€ monthly. At the same time, MultiSport partnerships remain strategically relevant, particularly for operators targeting the competitive range of roughly 45€–55€ per month.

Ultimately, the analysis indicates that meaningful whitespace opportunities still persist across Zagreb, particularly where favorable population density, competitive imbalance, and positioning potential intersect.